Medicare Advantage, a private alternative to traditional Medicare, offers extra benefits and low monthly premiums. However, prior authorizations and claim denials complicate this increasingly popular — and profitable — program for Medicare beneficiaries and their health care providers.

On a mid-November morning, Rick Cuddeford talked with Medicare-eligible Nebraskans about their options at the Saving Seniors Money office in Lincoln. His one-on-one discussions were timely, as the year’s open enrollment period ended on Dec. 7.

“We don’t push people one way or the other,” Cuddeford said. “Our job is to educate people about both options, and then whatever they are comfortable with, we go with for their coverage.”

Cuddeford said Saving Seniors Money — a group of independent insurance agents specializing in Medicare options — has helped over 5,000 households find Medicare options that work for them through educational seminars, one-on-one meetings and phone calls.

“When you do a good job, your name gets out there, and that’s how we grow,” Cuddeford said.

There are two paths that older Americans can take to secure health care insurance: traditional Medicare or a private Medicare Advantage plan.

Offering extra benefits and low monthly premiums, the lower upfront costs of Medicare Advantage plans can be appealing. But critics say choosing Medicare Advantage, which is seeing increased enrollment, can come with financial and health risks for many older Americans.

Jeremy Nordquist, president of the Nebraska Hospital Association, is wary of Medicare Advantage.

“With a lot of Medicare Advantage plans, you’re taking more of a financial risk,” Nordquist said. “You may pay less up front, but you’re taking a bigger financial risk as you age and move forward.”

Nordquist said private insurance companies, including Medicare Advantage plan providers, typically require approval before certain medical services are provided and covered. This can take time, and doctors and insurers don’t always agree. Nordquist said prior authorization procedures can delay timely access to care.

Around 2.8 million people across Nebraska, Iowa, Kansas and Missouri are on Medicare Advantage plans this year. Nationwide, 62 million people are eligible for Medicare Advantage. About 36 million are using it.

In a 2025 Nebraska Hospital Association survey, 83% of member hospitals reported care was denied to their Medicare Advantage patients. A majority of member hospitals also reported negative financial consequences related to dealing with Medicare Advantage companies, such as lost time for medical staff or low reimbursement rates.

Nordquist said seniors can also be stuck in the hospital when plans don’t cover skilled nursing or post-acute care.

About half of the Nebraska Hospital Association’s member hospitals no longer contract with certain Medicare Advantage plan providers. Around 10% of member hospitals – all in rural areas – no longer accept any Medicare Advantage plans.

“We’ve heard so many horror stories,” Nordquist said. “One that really sticks out to me was a cancer patient. It took the doctor seven months – the doctor knew, in their medical judgment, this service was medically necessary for the patient – seven months to get a cancer patient the treatment they needed, because the insurance company and Medicare-Advantage-plan-slash-insurance-company continued to deny that coverage.”

Providers also need to be “in network” with the Medicare Advantage plan, which could create a mismatch between an enrollee’s preferred providers and the plan’s covered providers. Most health systems accept traditional Medicare, giving those beneficiaries a larger pool of providers to choose from.

Nordquist said Medicare Advantage is better for seniors with few health issues.

“If you don’t think you’re going to need health care – great,” Nordquist said. “But very few seniors are healthy enough to avoid that, so they need to know these challenges up front.”

How it works

While traditional Medicare does not use prior authorization, a pilot program will test it out in six states starting in January 2026. A list of expensive services flagged as “unnecessary and often costly” will be subject to prior authorization under the pilot.

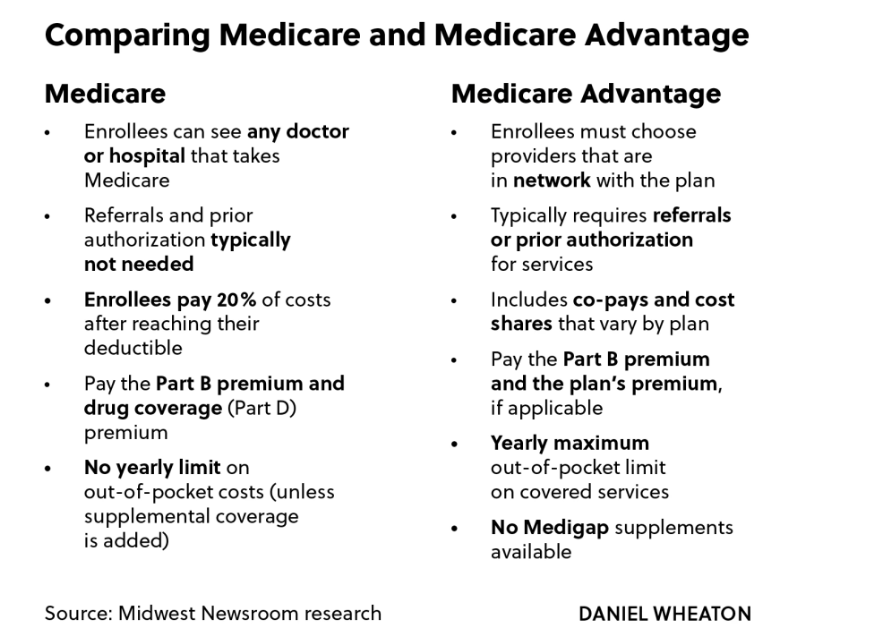

In traditional Medicare, provided by the federal government, enrollees typically start with Part A hospital insurance and Part B outpatient, home health and preventative care coverage. Enrollees can also add Part D drug coverage and “Medigap” supplement plans from private companies. Part A is free, Part B has an income-based monthly premium, and Part D drug and supplement plan costs vary.

Medicare Advantage enrollees pay their Part B premium and the plan’s monthly premium, which is typically free or low cost. Dental, vision or hearing coverage – which are not included with traditional Medicare – are commonly offered as extra benefits. Some plans even offer gym memberships or grocery vouchers.

However, unlike traditional Medicare, Medicare Advantage enrollees typically have co-pays and a maximum out-of-pocket amount tacked onto their coverage. Traditional Medicare enrollees pay 20% of their health care costs after they’ve met their deductible, unless they have a supplement that kicks in.

Cuddeford compared Medicare Advantage plans to the health insurance plans most people under age 65 are familiar with.

“Your health care insurance you have right now – it’s basically an Advantage plan,” Cuddeford said. “It works the same way. You probably have a deductible, then you probably have co-pays and cost shares up to a max out of pocket. That’s exactly what an Advantage plan is.”

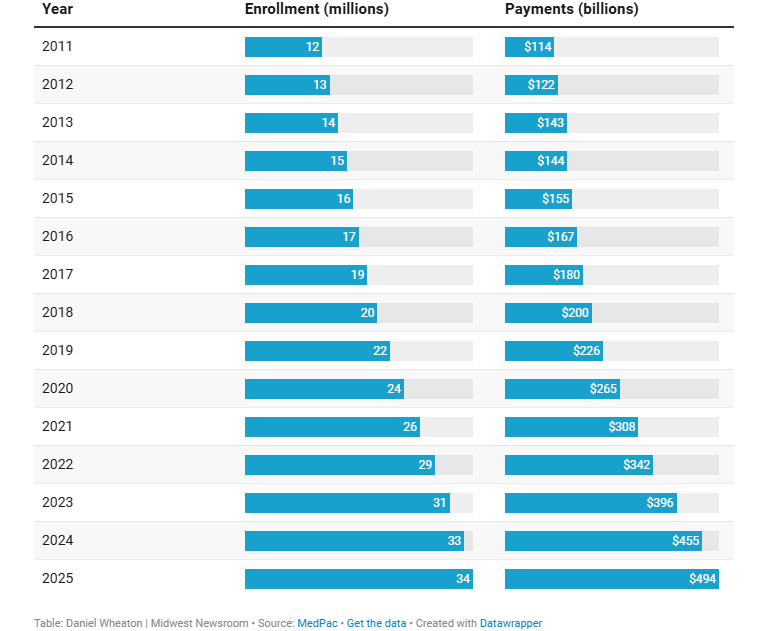

In 2011, 26% of Medicare beneficiaries were on a Medicare Advantage plan, according to a report from the Centers for Medicare & Medicaid Services (CMS). Now, in 2025, about 55% of Medicare beneficiaries use Medicare Advantage.

More people using Medicare Advantage

Enrollment in Medicare Advantage plans has increased steadily for more than a decade.

KFF is a nonprofit health education and policy organization. Jeannie Fuglesten Biniek, associate director of KFF’s program on Medicare policy, said it’s difficult to know how many claims are denied by Medicare Advantage insurers.

“Unfortunately, we don’t have data to really say how often there was a misalignment between what people’s providers, their doctors and their families thought that they needed and what the insurer said,” Fuglesten Biniek said. “We’ve just heard stories where people have faced these challenges at a time when they’re actually pretty vulnerable.”

The Centers for Medicare & Medicaid Services does track how often claims are denied on plans offered through Affordable Care Act health insurance exchanges, but not all Medicare Advantage plans are required to report why they denied claims.

“There’s just a disconnect or a difference in what is required in the different insurance markets,” Fuglesten Biniek said.

Fuglesten Biniek said Medicare Advantage plan providers use prior authorization, referrals and provider networks to control costs.

“Most insurers will tell you that it is a tool that they need in order to make sure that people don’t get inappropriate care and there’s not wasteful spending,” Fuglesten Biniek said. “But they have talked about doing it better, using it for fewer services that are really the higher-risk services.”

'A viable offer'

With free or low-cost monthly premiums, Cuddeford said many of his clients choose Medicare Advantage plans as a more affordable alternative to steadily rising Medicare supplement costs.

“I had a gentleman call me. It’s been a couple years ago now,” Cuddeford said. “It’s the biggest one I ever found. His supplement was $750 a month,” Cuddeford said.

When the man said he would soon have to choose between health care and putting food on the table, Cuddeford recommended a Medicare Advantage plan.

“He has not had any medical issues in the last two years. Nothing major to speak of,” Cuddeford said. “He has saved nearly $20,000 by being on a Medicare Advantage plan.”

With Part B premiums increasing 9.7% next year, a standard Medicare enrollee’s bill can add up quickly. Supplement premiums can range from $30 to well over $600. As the cost of traditional Medicare rises, a larger share of Americans are turning to Medicare Advantage.

“All of a sudden, it’s a viable offer, especially when that supplement premium is unaffordable for someone who’s living off Social Security,” Cuddeford said.

The federal government pays Medicare Advantage plan providers per person each month to distribute an enrollee’s Medicare benefits. Cuddeford said those payments used to be lower, but as enrollment climbed, so did government payments. More insurance companies entered the Medicare Advantage market, using television commercials, mailers and online advertisements to push extra benefits and $0 premiums while leaving out crucial details like network requirements and co-pay information.

“It’s easy to sell free,” Cuddeford said.

The Saving Seniors Money team is made up of independent insurance agents that contract with multiple insurance companies to sell their products.

According to Centers for Medicare & Medicaid Services data, agent commissions for selling a Medicare Advantage plan to a first-time enrollee ranged from $92 to $780 in 2025, though caps on commission amounts vary by state. Commissions for Medicare Advantage plans and Part D plans are regulated and capped by Centers for Medicare & Medicaid Services, but this is not the case for Medicare supplement providers that cover copays and deductibles under MediGap.

According to KFF, the average monthly premium of a Medigap supplement in 2023 was $217, making $520 an average agent’s commission. Medigap supplement commissions for a first-time enrollee are typically around 20% of the plan’s annual premium, which can vary by insurance provider and plan type. Commissions go down each year that an enrollee stays on a Medicare Advantage, Part D or supplemental plan.

A push for transparency

In 2024, the federal government spent $1.1 trillion on the Medicare program as a whole. Around $494 billion was paid out to Medicare Advantage plan providers – nearly 45% of total Medicare expenditures. That dollar amount has more than quadrupled since 2011.

Payments will rise again this year. In April, the Centers for Medicare & Medicaid Services announced rates would rise 5.06% for 2026.

When Medicare Advantage was introduced in 1997 as Medicare+Choice, it was intended to provide more options to seniors while saving the federal government money through partial privatization of the Medicare program.

However, Great Plains Health CEO Ivan Mitchell doubts the program’s original intentions are being carried out.

“I think we’re to a point where we need to start over and scrap the program,” Mitchell said.

Recently, Centers for Medicare & Medicaid Services’ Medicare Payment Advisory Commission reported that payments to Medicare Advantage plans are about 20% higher than spending for similar enrollees in traditional Medicare, adding up to $84 billion in payments to insurance companies for 2025 alone.

KFF’s Fuglesten Biniek said extra benefits offered by Medicare Advantage plans could partially account for the higher cost.

“It’s not exactly apples to apples in terms of what the person is getting, and it is quite possible that the higher spending and Medicare Advantage is delivering value to the enrollee that justifies the cost,” Fuglesten Biniek said.

Studies have been commissioned by insurance companies or groups with a vested interest in the success of Medicare Advantage. There is not unbiased or comprehensive data on how Medicare Advantage plans’ extra benefits affect enrollee health.

Fuglesten Biniek said the government is also aware of prior authorization concerns.

“[Health and Human Services] did an analysis of this and actually found that Medicare Advantage plans were denying services in cases where it was likely traditional Medicare would have covered it,” Fuglesten Biniek said. “[Centers for Medicare & Medicaid Services] issued new regulations clarifying that they were supposed to be covering services in these cases.”

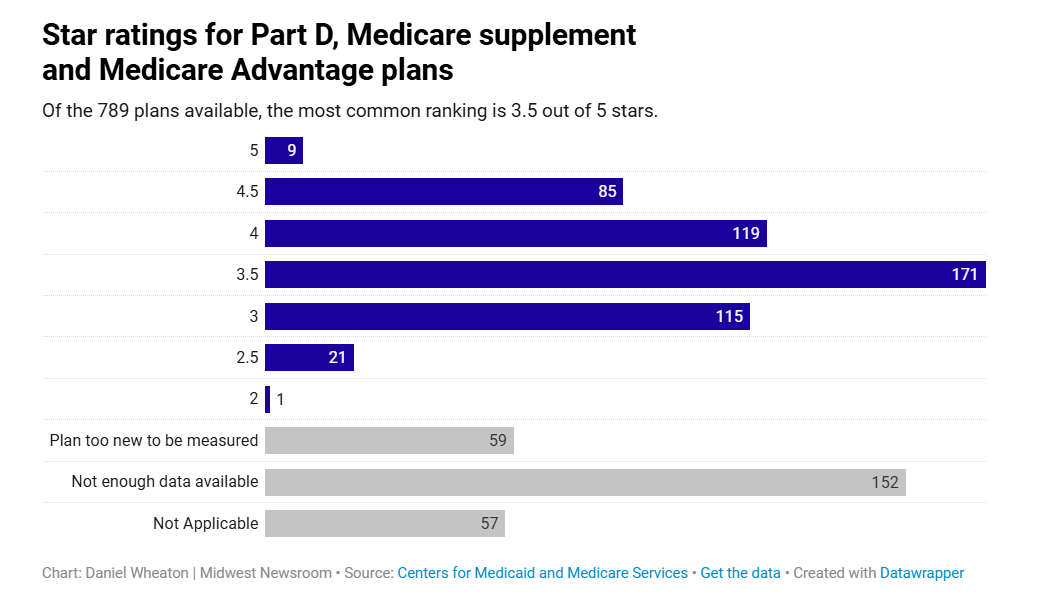

The Centers for Medicare & Medicaid Services uses “a five-star rating system” to rate plan quality and consumer satisfaction of Part D, Medicare supplement and Medicare Advantage plans, based on 40 measurement criteria and consumer satisfaction. Plans with high star ratings get bonus payments from the government. Plans with low star ratings can be sanctioned and not allowed to enroll new members.

For 2026, about 40% of plans are rated at four or more stars, according to a CMS fact sheet. Weighted by enrollment, 64% of enrollees are currently on plans that earned four or more stars as their 2026 rating.

Notably, a Centers for Medicare & Medicaid Services rule from 2023 decreased the weight of patient experiences for calculating star ratings. In 2024, Centers for Medicare & Medicaid Services was the subject of several lawsuits from Medicare Advantage providers alleging inaccurate or unfair calculations of star ratings.

A practice called “upcoding” also factors into higher government payments. If a plan has many patients with severe medical issues, chronic conditions or complications, the plan has a higher “risk score.” The higher the risk score, the higher the payments from the government.

“One of the ways in which plans collect diagnosis codes to increase their risk scores is through something called chart reviews, where they can take an artificial intelligence and they go through all the medical records and find diagnoses that were not submitted as part of that encounter with the provider, but they think there’s evidence of,” Fuglesten Biniek said.

MedPAC reported Medicare Advantage plan risk scores were 17% higher on average compared with traditional Medicare beneficiaries. While Centers for Medicare & Medicaid Services is required by law to reduce MA plan risk scores to bring payments closer to traditional Medicare costs, risk scores are still high after adjustment.

Those chart reviews cost the government $24 billion in 2023, around 6% of total Medicare Advantage payments that year.

“That started to get a lot of bipartisan attention,” Fuglesten Biniek said. “I don’t know what that will mean in terms of specific policy changes, but it’s an area that both people in the [Trump] administration and Congress are interested in, and both Republicans and Democrats are interested in. It’s not often that something has all of those things aligned.”

Sen. Chuck Grassley of Iowa criticized Medicare Advantage earlier this year following a February Wall Street Journal report on a Department of Justice investigation into UnitedHealth Group’s billing practices.

Kansas Sen. Roger Marshall introduced a bill in May increasing transparency by requiring Medicare Advantage plans to report to the government how many claims are denied each year. The bill has 63 bipartisan co-sponsors, including all four Nebraska and Missouri senators, Iowa Sen. Joni Ernst and Kansas Sen. Jerry Moran. An identical version was introduced in the House with widespread support, but no action has been taken on the House or Senate version since May.

A “No Upcode Act” has bipartisan support in the Senate, according to Fuglesten Biniek, and a House member proposed a bill to extend ACA tax credits by changing how risk scores are calculated.

Centers for Medicare & Medicaid Services Administrator Dr. Mehmet Oz has also expressed problems with upcoding and lack of transparency from Medicare Advantage plans. Oz was previously a staunch supporter of Medicare Advantage on the “Dr. Oz Show” and throughout his failed bid for the U.S. Senate in 2022.

Tough for health providers

Issues of delayed care, prior authorization and time lost to paperwork have led to tough decisions for health care providers. And all the while, more people are learning about Medicare Advantage.

“We’ve started to see more advertising, more outreach, more engagement in rural areas, and that, I think, is creating some of the pushback from our members saying it’s bad for patients,” said Nordquist, president of the Nebraska Hospital Association. “When a big, out-of-state insurance company comes in and tries to force us to take a contract, you don’t, as a small hospital, have any real leverage to negotiate on that, other than it’s take it or leave it.”

Major health systems such as Mayo Clinic and Scripps have stopped accepting Medicare Advantage plans. Across the country, Becker’s Hospital Review reports 33 health systems have announced they will not accept some or all MA plans past 2025, including Iowa’s MercyOne, Iowa Specialty Hospitals and Clinics, Kansas-based LMH Health and Kimball Health Services in Nebraska.

Great Plains Health, a small health system in North Platte, announced it would no longer take any Medicare Advantage plans starting on Jan. 1, 2025.

“The largest employer in our community, at the end of 2023, sent a letter to their retirees saying that they were going to switch them all to a Medicare Advantage plan that we were not in network with, versus a traditional Medicare plan with a supplement,” Great Plains Health CEO Ivan Mitchell said.

Mitchell said Great Plains Health had already seen issues during its limited adoption of Medicare Advantage plans. The employer assured the health system that patients could be served on an out-of-network basis with no prior authorizations.

“We said, ‘OK, well, we don’t really believe you, but we’re going to go ahead and give it a shot,’” Mitchell said.

Mitchell said problems started almost immediately. As an example of Great Plains Health’s issues with Medicare Advantage plans, he shared a patient’s story.

The patient had an infection that went septic. The patient was put on a ventilator at Great Plains Health, and eventually, their condition improved. For a full recovery, the patient needed rehabilitative care. In order to get a spot at the rehabilitation hospital, the patient needed prior authorization from their Medicare Advantage plan.

Care was denied multiple times. Doctors sat on hold. The patient stayed an extra six weeks at Great Plains Health.

“If you look at keeping this patient here an additional six weeks, that was an additional 10 patients that could have been admitted to our hospital that were not able to be admitted here,” Mitchell said. “And the next closest hospital to us that provides the same level of care is 100 miles away.”

Mitchell said that wasn’t the only case. As more issues arose, he said doctors were spending precious time that could be used caring for patients on the phone, fighting with the insurance company.

“According to statute, they are supposed to follow traditional Medicare guidelines,” Mitchell said. “I can tell you that they don’t, and there are clearly patients that would have received care that were denied it and not given any rationale that said they didn’t meet Medicare guidelines.”

After Great Plains Health stopped taking Medicare Advantage plans, the Centers for Medicare & Medicaid Services granted a special enrollment period to patients so they could enroll in traditional Medicare with a supplement or find a different option. Great Plains Health still accepts Medicare Advantage patients who need emergency care, but those patients won’t be able to schedule regular appointments.

Even with all the turmoil behind the scenes, Mitchell said, denying Medicare Advantage patients was a tough decision to land on.

“Running a hospital, the last thing you want to do is not accept care,” Mitchell said. “And it does really bother me that there’s around 400 members in our county that can’t access Great Plains Health for their routine specialty care. It looked to me to be a choice of being shot or stabbed, and I think we had to pick the best of the worst options.”

Generally, Mitchell said, Great Plains Health can serve its community better with space and time freed up from dealing with Medicare Advantage insurers. He doesn’t see a future where Medicare Advantage works for everyone.

“We basically raided the Medicare trust fund with these for-profit insurance companies that, in my opinion, have been extremely unethical in what they’ve done,” Mitchell said.

“Running a hospital, the last thing you want to do is not accept care,” Mitchell said. “And it does really bother me that there’s around 400 members in our county that can’t access Great Plains Health for their routine specialty care. It looked to me to be a choice of being shot or stabbed, and I think we had to pick the best of the worst options.”

Generally, Mitchell said, Great Plains Health can serve its community better with space and time freed up from dealing with Medicare Advantage insurers. He doesn’t see a future where Medicare Advantage works for everyone.

“We basically raided the Medicare trust fund with these for-profit insurance companies that, in my opinion, have been extremely unethical in what they’ve done,” Mitchell said.

A way forward

Between rising Medicare supplement costs and the risks of a Medicare Advantage plan, it can be tough for seniors to make the right decision. To help, every state has a State Health Insurance Assistance Program that provides free and unbiased information and consultations about Medicare options.

“We will answer questions and help an individual really understand what scenario A versus scenario B may entail for their personal situation,” Nebraska's State Health Insurance Assistance Program administrator Jonathan Burlison said. “So really, it is a decision that an individual is responsible for. It is their health insurance.”

Burlison recommended Medicare.gov as a comprehensive, unbiased resource for choosing a plan.

“Medicare.gov provides explanations of a plan’s rating within the plan details there,” Burlison said. “One can basically see various factors used to determine the plan’s ratings, which include keeping folks healthy, managing chronic conditions, members’ experience, if offered, drug coverage.”

A provider search tool on Medicare.gov allows enrollees to search which doctors are in-network before they choose a Medicare Advantage plan. Medicare Advantage plans can also change from year to year, requiring seniors to review plans annually. Providers or health systems can leave plans, or the insurance company can move them out of network.

Even with unbiased government tools, state-sponsored help and volunteer groups, Burlison said, some seniors still don’t learn about the risks of Medicare Advantage before signing a contract.

“Medicare’s individual insurance,” Burlison said. “What works well for friends, family and neighbors potentially isn’t a good fit for the individual.”

Should a senior make the wrong personal choice, there are some course correction options.

According to Burlison, if a senior used the Medicare.gov provider search tool to confirm their doctor was in network, then finds their doctor is out of network, Centers for Medicare & Medicaid Services will grant the person a “special enrollment period” to choose a different option.

Special enrollment periods are granted under some other specific circumstances. The first time a person tries a Medicare Advantage plan, they have a year to switch back, free of cost.

However, special enrollment periods aren’t always guaranteed. Even during the annual enrollment period from October to December, switching back to traditional Medicare can require the enrollee to pay medical underwriting costs to make up the difference they would have spent on traditional Medicare supplement premiums.

Through the constantly shifting Medicare landscape, Cuddeford and the Saving Seniors Money team is focused on helping people make the right choices for their physical and financial health.

“There’s so many factors involved here – what a person can afford for their coverage versus the doctor side of it, the network side of it,” Cuddeford said. “So what do you do? You do the best you can with the information you have at hand.”

Cuddeford said taking the time to sit down with a client and learn their situation goes a long way in creating better outcomes for those on Medicare – traditional or Advantage.

“We have a pretty large block on Medicare Advantage plans,” Cuddeford said. “The majority of our business does sit in the Medicare supplement world, but the ones that are on Advantage plans, I’d say 99% of them report a positive experience back to us.”

Though Medicare Advantage works out for most of his clients, Cuddeford still leans toward traditional Medicare with a supplement. However, he understands personal finance’s role in health care decisions.

“In a perfect world, if I could keep my clients on traditional Medicare with a Medicare supplement that was within their budget and just add a simple Part D drug program, honestly, that would be my preference,” Cuddeford said. “That’s generally where 99% of our clients start off with when they’re brand-new to Medicare. But as they get older and those prices become unaffordable to them, we’re really kind of left with no choice, and it’s all financially driven for our clients.”

As open enrollment wraps up on Dec. 7, Cuddeford is happy knowing he helped seniors confidently make a decision.

“We use the word ‘comfortable’ a lot,” Cuddeford said. “We want our clients to choose whatever they are comfortable with. And if they’re comfortable and they’re happy, then we’re happy.”